History of the Swiss franc: from Napoleon to a global safe-haven currency

- Strong currency VS weak currency: what are the differences?

- From its origins to unification: how was the Swiss franc born?

- The evolution of the Swiss franc in the 20th century

- Why did the Swiss franc become a safe-haven currency?

- The political and economic factors behind its solidity

- Swiss franc, euro and dollar: evolution and comparisons

- Summary of reasons why the Swiss franc is a strong currency

- Swiss franc and foreign capital: a pillar of its stability

Would you like to understand why the Swiss franc (CHF), that strong currency and the ultimate safe-haven asset, is holding up so well against global turmoil? The CHF hasn’t always been such a powerhouse.

• The Swiss franc doesn't owe its strength to chance: it's the result of two centuries of monetary discipline and rigorous political choices.

• Historic neutrality, gold backing, controlled inflation and a proactive SNB: four factors that explain why investors worldwide take refuge in CHF during crises.

• Against the euro and the dollar, the franc has kept appreciating over the long term, with only one devaluation episode, in 1936.

- Strong currency VS weak currency: what are the differences?

- From its origins to unification: how was the Swiss franc born?

- The evolution of the Swiss franc in the 20th century

- Why did the Swiss franc become a safe-haven currency?

- The political and economic factors behind its solidity

- Swiss franc, euro and dollar: evolution and comparisons

- Summary of reasons why the Swiss franc is a strong currency

- Swiss franc and foreign capital: a pillar of its stability

Its history is a fascinating tale, starting from the monetary fragmentation of the Napoleonic era through to the establishment of a world-renowned currency.

Today, a robust economy, low debt and the strategic management of the Swiss National Bank (SNB) guarantee its solidity.

Source : ProRealTime Web

But the true strength of the franc lies in the lessons drawn from its past.

Let’s go back to its origins. B-sharpe, your exchange partner, shows you today how and why the Swiss franc became a pillar of stability, what mechanisms support it, and how it compares against the euro and the dollar.

The history of the Swiss franc gives you the keys to decoding the foreign exchange market and optimising your transactions with us.

…Before diving into the depths of the Swiss franc’s history, let’s first clarify what a “strong currency” is.

Strong currency VS weak currency: what are the differences?

The notion of a strong currency is entirely relative. A currency can be ‘strong’ relative to one currency, and ‘weak’ relative to another.

- Take the EUR/CHF pair as an example (in other words, what one euro is worth after conversion into Swiss francs).

You had to spend around 1,219 Swiss francs at the start of 2012 to obtain 1000 euros, but today it only takes 1,035 francs to obtain the same amount.

While both currencies can, in absolute terms, be considered strong, the Swiss franc has won the match against the euro over the last decade with a positive movement in the exchange rate against the single currency.

- Another example:

Over the same period, you had to spend around $1,270 to obtain €1000 in 2012, whereas today you need to spend just a little under $1,134 to have the same amount.

From its origins to unification: how was the Swiss franc born?

The Swiss franc under the Napoleonic era

Before the introduction of a modern national currency, Switzerland was a genuine financial maze. The Old Swiss Confederacy (until 1798) had no concrete monetary unit.

Most of the thirteen cantons minted their own currency.

This led to extreme diversity: 319 types of coins coexisted alongside numerous foreign currencies, making national trade complex.

It’s worth knowing that the history of the Swiss franc is closely tied to French influence.

The short-lived unity of the Helvetic Republic (1798-1803)

The French invasion of 1798 and the creation of the Helvetic Republic put an end to the fragmentation.

Inspired by the centralised French model, the new Republic made a radical and unprecedented decision: to impose a single currency across the entire territory. This is when a Franc de Suisse made its first official appearance, putting a temporary end to the monetary “every man for himself” among the cantons.

The return to fragmentation under the Mediation (1803-1848)

This period of unity was short-lived.

In 1803, Napoleon Bonaparte intervened with the Act of Mediation, dismantling the centralised government.

Switzerland once again became a confederation. The immediate financial consequence is a step backwards: each canton regains its sovereignty and the right to mint its own currency once more.

The monetary system becomes fragmented once again.

Faced with the persistent chaos of this cantonal diversity, six cantons (including Bern, Vaud and Basel) signed a monetary concordat in 1825. This alliance aimed to harmonise the types of coins and their value within their territories.

Although limited, this initiative marks the first concrete attempt, led by the cantons themselves, to restore financial coherence (Source : Historical Dictionary of Switzerland ).

The path to federal monopoly: the 1850 Monetary Act and the Swiss federal state

The real turning point comes after the Sonderbund War.

In 1848, the new Federal Constitution enacts a fundamental change: the monopoly on minting currency is granted to the Confederation.

This political decision ends cantonal monetary sovereignty and legitimises the unification process.

The next step, the establishment of the Swiss franc as we know it, then becomes inevitable.

Between 1851 and 1852, the federal state withdrew more than 66 million old coins of the 319 varieties in order to clean up the market ahead of the 1850 Monetary Act.

In its early days, the new Swiss franc was moreover set at parity with the French franc (known as the “franc germinal”), confirming a major historical influence and guaranteeing initial exchange rate stability.

💡 Good to know :

The 1803 Act of Mediation was not aimed solely at currency, but at the very survival of the state. The centralisation imposed by the Helvetic Republic (1798) had proven impracticable due to Switzerland’s deep linguistic, religious and cultural differences.

The situation degenerates into civil war (the “war of the sticks”) when the federalists, supporters of cantonal sovereignty, gain the upper hand over the central government.

It is in response to this implosion that Napoleon intervenes as “mediator”, imposing a new structure. He restores autonomy to the cantons, but ensures that France retains a clear influence over Switzerland’s economic and foreign policy.

The Mediation regime relied entirely on this Napoleonic domination and collapsed at the same time as the Empire, in 1813.

So, what happens to the Swiss franc from the 1850 Monetary Act to the First World War?

The franc’s new stability quickly encourages Switzerland to integrate into the dominant European monetary system.

The Latin Monetary Union (LMU)

In 1865, Switzerland signs an agreement with France, Italy and Belgium to create the Latin Monetary Union (LMU) (Greece would join in 1868).

Source : Historical Dictionary of Switzerland

This union is a practical response to the turbulence caused by gold discoveries in America and Australia, which threatened the balance of precious metals.

The LMU is based on bimetallism (the joint use of gold and silver) with a fixed ratio between the two precious metals (1/15.5). The system aligns with the characteristics of the 1803 French franc.

The countries commit to minting gold coins and silver écus with a purity of 900/1000, and small-denomination coins with a purity of 835/1000.

The most direct effect for Swiss trade is mutual acceptance.

The currencies of the five member countries can circulate freely and are legal tender in all States of the Union, reinforcing Switzerland’s integration into the French monetary zone.

Towards the Gold Standard and the Swiss National Bank

The LMU is quickly confronted with challenges.

The adoption of the gold monometallic standard by the German Empire in 1871, coupled with an increase in global silver production, leads to a depreciation of the white metal.

To counter this phenomenon, the countries of the Union limit, then suspend the minting of silver coins in 1880. The system shifts de facto to the Gold Standard alone.

Alongside these efforts to standardise coins, the issuance of banknotes remains fragmented among cantonal banks for a long time.

It was not until 1907 that the State completed its monetary centralisation by granting the monopoly on note issuance to the Swiss National Bank (SNB)

(Source : EPFL PRESS)

The First World War will effectively put an end to the free circulation of LMU currencies. But the Swiss franc emerges strengthened, having already established its value on the international stage.

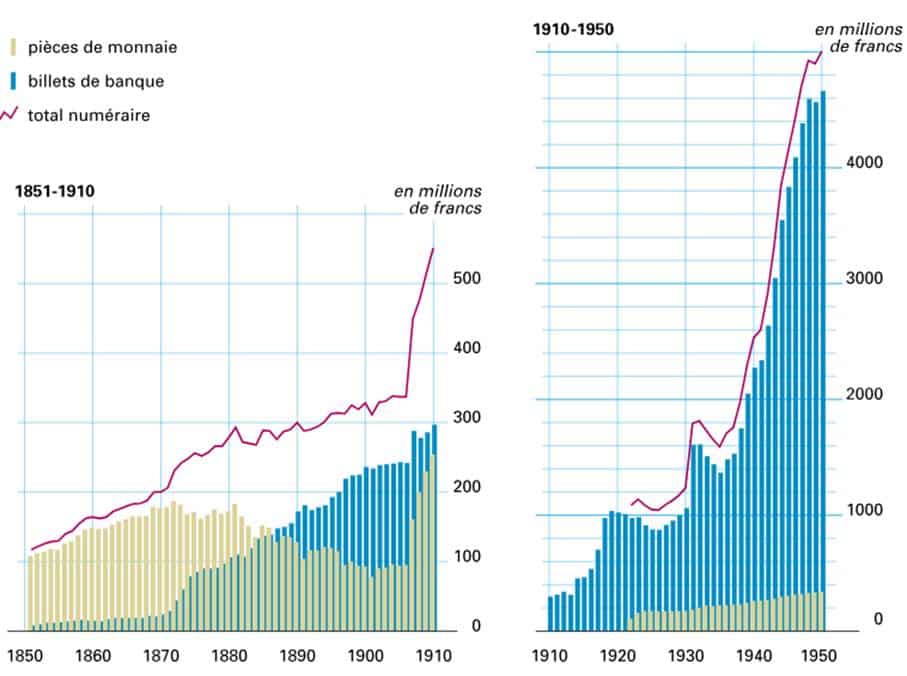

Monetary circulation 1851-1950

Sources: C. Grüebler, Die Geldmenge der Schweiz 1907-1954, 1958; H. Ritzmann-Blickenstorfer, ed., Historical Statistics of Switzerland, 1996, pp. 805-806 © 2003 HLS and Marc Siegenthaler, Bern.

The evolution of the Swiss franc in the 20th century

1920-1945: gold standard, crises and the franc’s affirmation

The interwar period forges the reputation of the Swiss Franc (CHF) as a safe-haven currency.

While European currencies experience a period of great instability — marked by the hyperinflation of the German mark in the Weimar Republic, which illustrates a spectacular loss of value — the Swiss franc stands out for its solidity.

This strength results mainly from Switzerland’s maintenance of the gold standard.

By retaining a direct link with the yellow metal, the currency massively attracts foreign capital seeking safety.

But this dearness also has negative consequences for the country’s economy.

- The impact on exports: A franc that is too strong severely penalises the Swiss economy, largely oriented towards exports.

- The employment crisis: The impact of the crisis is such that by the mid-1930s, unemployment affects more than 20% of the working population.

Faced with this situation, the Confederation is forced to act.

The Federal Council reduces the weight of the franc from 0.290032 g of fine gold to an amount to be set between 0.190 g and 0.215 g on 26 September 1936.

This is the first and only devaluation of the Swiss franc, decided to support competitiveness (Source 2).

During the Second World War, Switzerland further strengthens its foundations by selling raw materials to Germany in exchange for large quantities of gold.

These two decades (1920-1945) definitively establish the basis for the CHF’s future solidity.

Switzerland, the Swiss franc and foreign capital

Countries with a so-called strong currency all share the same characteristic: they attract capital from foreign investors. The more foreign capital flows in, the stronger the currency becomes.

In 2020, more than 1216 billion Swiss francs of foreign investment were found on Swiss soil. In turn, Switzerland invested more than 1460 billion CHF worldwide.

Switzerland is one of the world’s leading investors abroad. But in 2019 and 2020, amid the health crisis, the country’s companies repatriated 54 and 34 billion Swiss francs respectively, enough to support the Swiss franc on the foreign exchange market.

Bretton Woods and the move to floating exchange rates

At the end of the war, the world monetary order is redefined by the Bretton Woods agreements (1944). This system anchors currencies to the US dollar, itself tied to gold. Switzerland, as a matter of political choice, refuses to join (Source 1). Despite this official non-participation, the Swiss franc remains among the most robust currencies in the world.

The Bretton Woods system collapses in 1971, ushering in the era of floating exchange rates, where the value of currencies is now determined by the free play of supply and demand on the markets (Source 1).

- Immediate consequence: The Swiss economy, already in good health, attracts a massive inflow of foreign capital seeking safety.

- Problem for businesses: This movement triggers a fresh appreciation of the franc. Industrial sectors, particularly those focused on exports, again face difficulties, leading to rising unemployment.

The Swiss National Bank (SNB) is forced to intervene to control the value of its currency.

The 1970s oil shock and the 1990s monetary crisis

The oil shocks of the 1970s accelerate the pressure on currencies. Despite the measures put in place by the SNB to curb its appreciation, the Swiss franc continues to rise.

The situation worsens with liquidity management difficulties. After the 1987 stock market crash, the SNB injects liquidity, but fails to control the long-term effects (Source 3). The construction and real estate sectors enter a speculative overheating.

- SNB’s reaction: To curb inflation and speculation, the SNB raises its interest rates.

- The recessive effect: This aggressive rise plunges the economy into a strong recession that characterises most of the 1990s.

The 1990s therefore remain economically difficult, notably due to a rate cut deemed too late (Source 3). The notable point is that, despite these domestic difficulties, the Swiss franc maintains its value against the majority of other international currencies.

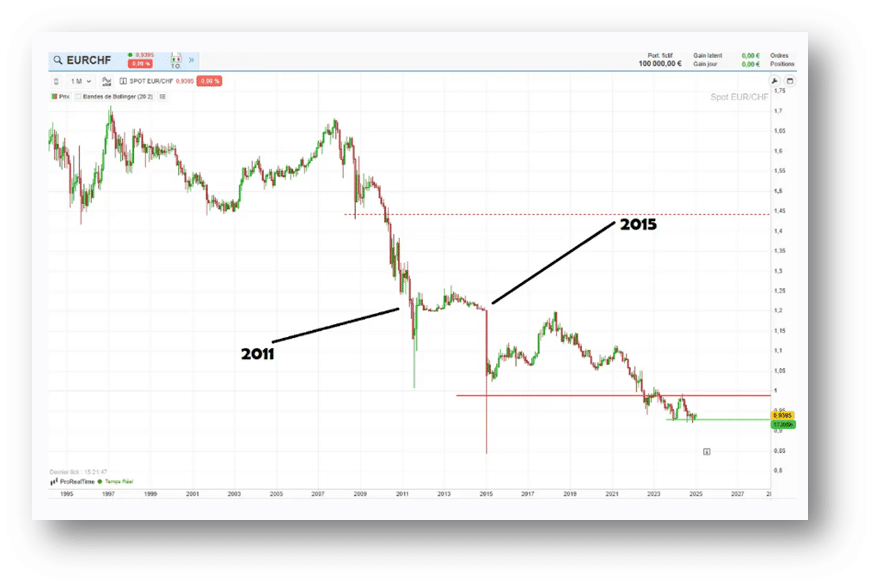

The minimum exchange rate in response to the 2008 crisis

The 2008 financial crisis spectacularly reaffirms the safe-haven status of the Swiss franc.

In 2010, the SNB responds to the crisis by lowering its interest rates to zero and flooding the market with liquidity to protect the banking system.

However, the CHF appreciates sharply against the euro and the dollar, threatening the competitiveness of Swiss exports.

To protect domestic businesses, the SNB takes a drastic measure:

- The minimum exchange rate: The SNB establishes a minimum exchange rate against the euro (EUR/CHF), which it commits to defending through massive interventions.

- The abolition: This floor is maintained for several years before being suddenly abandoned in 2015. The abolition triggers a global monetary “shock”, as the franc appreciates instantly.

These interventions, whether the 1936 devaluation or the 2015 floor, confirm that the franc’s stability is regularly put to the test by its own success and its role as a safe-haven currency.

Why did the Swiss franc become a safe-haven currency?

The safe-haven status of the Swiss franc (CHF) is not due to chance, but to a long historical and institutional process. Long considered an “appendage” of the French franc in its early days, the CHF established itself in the 20th century as a stable and highly sought-after investment currency.

This solidity results from several factors that create lasting confidence among investors seeking to protect their capital, particularly in periods of uncertainty:

- Historical and Political Stability: The country has built up an immense capital of trust by having been spared major conflicts since the mid-19th century and by demonstrating strong political and social stability.

- Long-standing Link with Gold: The franc has historically been tied to gold, which established its reputation for stability. Even after abandoning the gold standard, Switzerland continued to hold substantial gold reserves.

- Low Inflation: Persistently low inflation is a key economic factor.

- Independence and Fiscal Discipline: Rigorous discipline in terms of fiscal and monetary stability adds to a strong will for independence.

These combined elements make the Swiss franc a preferred choice when political uncertainties or international conflicts increase, as it is perceived as a shield against global instability.

The political and economic factors behind its solidity

The solidity of the Swiss franc rests on institutional mechanisms and tangible economic realities, often managed proactively:

The Central Role of the Swiss National Bank (SNB)

The Swiss National Bank (SNB) is the main actor in maintaining CHF stability.

- Rigorous Monetary Policy: The SNB commits to ensuring price stability while taking overall economic developments into account. It uses tools such as the policy rate and interventions on the foreign exchange market to control inflation and stabilise the economy.

- Independence and Proactivity: The SNB is one of the few central banks in the world that also operates as an investment fund, buying bonds and shares of global companies. It adjusts its currency reserves and interest rates proactively to influence the value of the franc.

- Crucial Independence: The autonomy of the SNB’s monetary policy from fiscal policy is a pillar of its credibility, protecting the currency from short-term political considerations.

The Economic Confidence Factors

- Gold Reserves: Switzerland is a major gold holder, regularly ranking among the 10 largest holders in the world. It holds around 1,040 metric tonnes of gold, representing about 5% of its total reserves (which also include foreign currency, bonds and equities). These reserves reinforce investor confidence.

- Robust Economy and Low Inflation: Generally robust Gross Domestic Product (GDP) growth and a controlled level of inflation attract capital. A dynamic, expanding economy reinforces confidence and can lead to an appreciation of the CHF.

- Geopolitical Factors: The Swiss franc’s safe-haven status is also reinforced by geopolitical factors. Any international crisis or political uncertainty mechanically increases demand for the CHF.

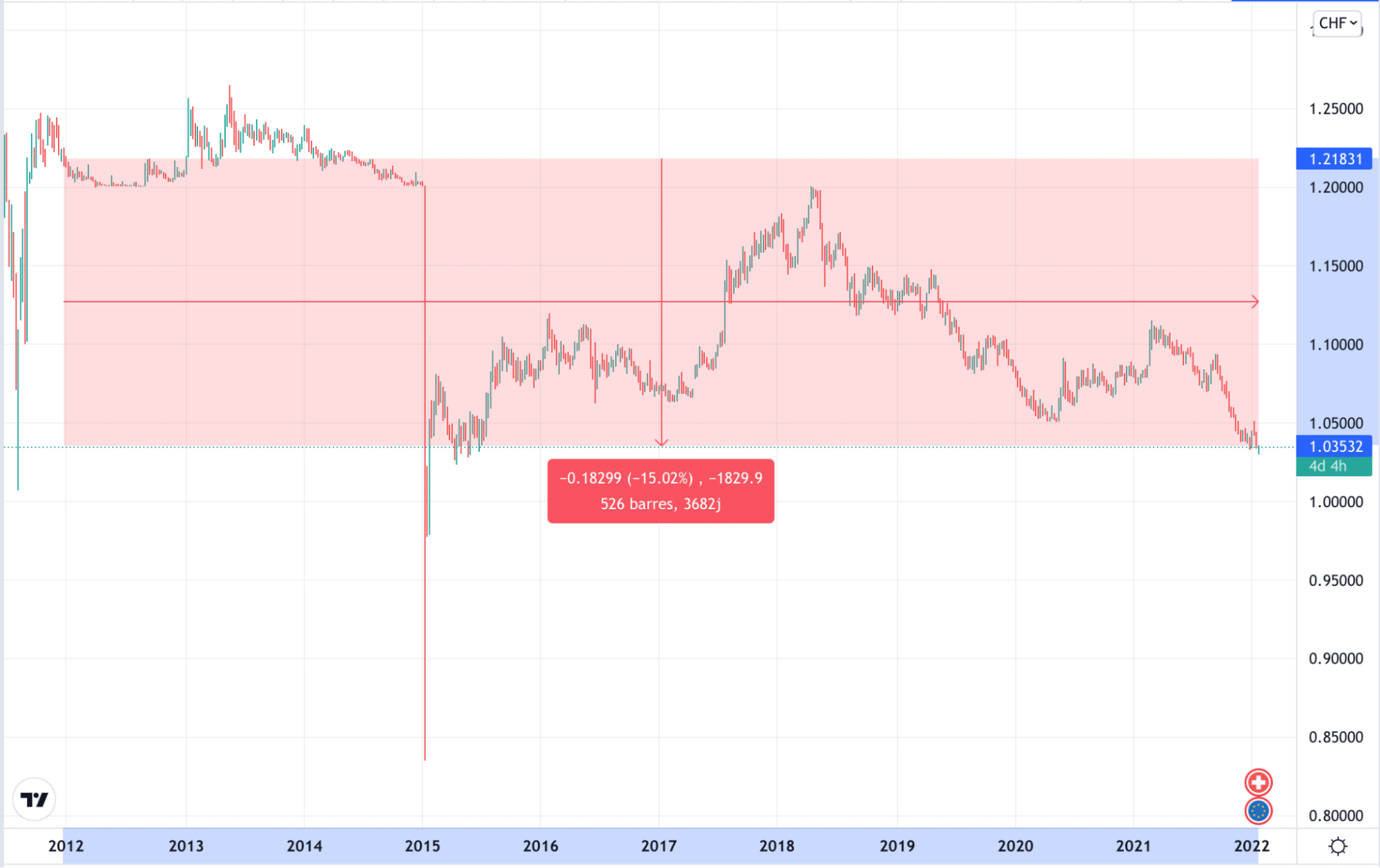

Swiss franc, euro and dollar: evolution and comparisons

The evolution of the Swiss franc against the two main world currencies highlights the strength and specificities of the CHF.

Swiss Franc against Euro (EUR)

The most volatile interaction of the Swiss franc is observed against the euro.

- The Minimum Exchange Rate (2011–2015): To protect its economy from the effects of an overly strong franc, the SNB established a minimum exchange rate of CHF 1.20 per EUR 1 on 6 September 2011.

- The Abandonment (2015): The SNB put an end to this floor on 15 January 2015, triggering a “tsunami” on the markets. The euro fell below parity, reaching a historic low. This decision, although bold, demonstrated the SNB’s ability to adapt quickly to changing conditions.

- Fluctuations: Fluctuations in the EUR/CHF exchange rate are often marked by divergent monetary policies between Switzerland and the Eurozone, with significant variations being common.

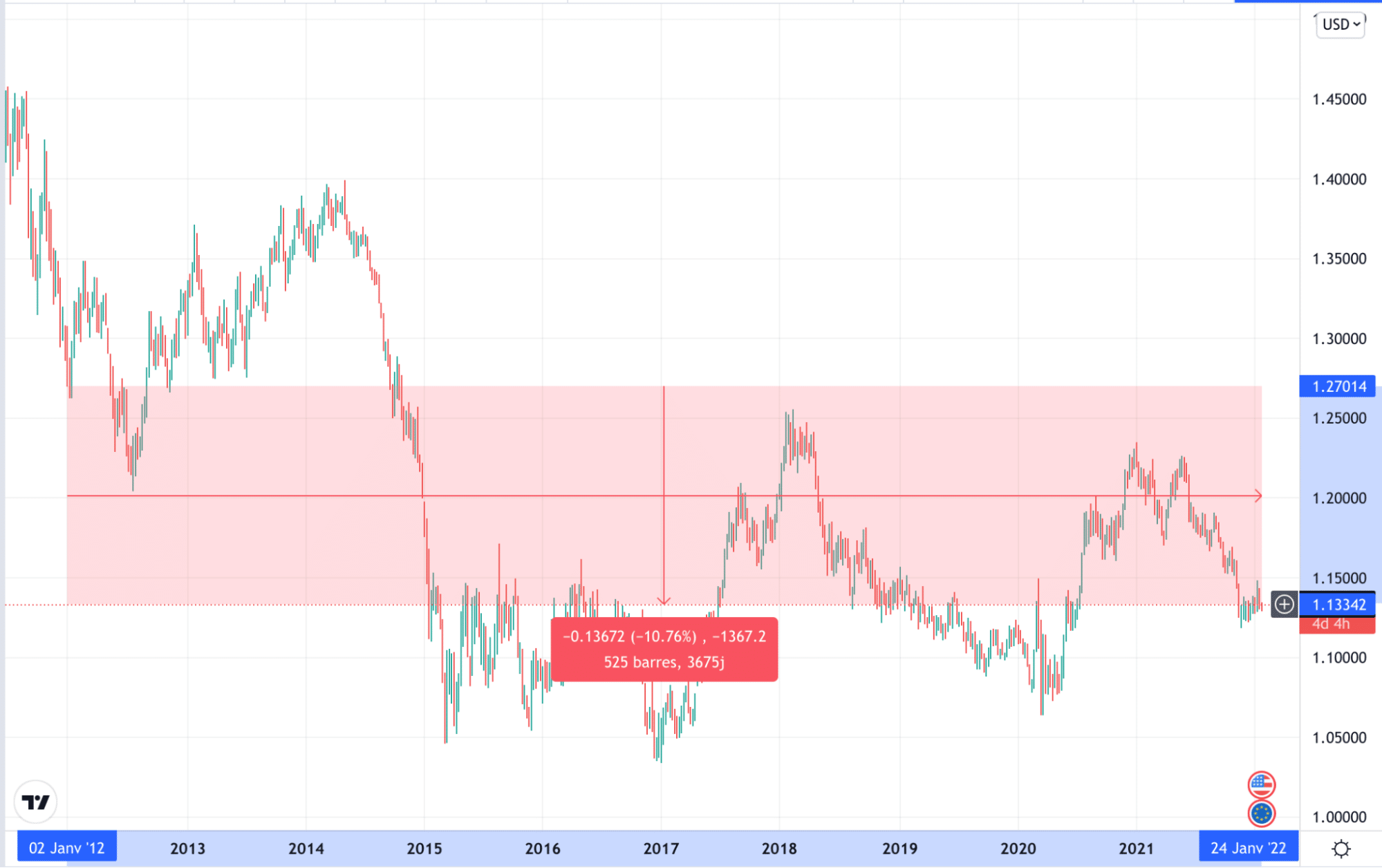

Swiss Franc against Dollar (USD)

Against the dollar, the Swiss franc has shown historical strength and relative recent stability.

- Historical Appreciation: The US dollar, which was worth CHF 5.18 in 1914, was already trading barely above CHF 0.80 in 2011 (according to available historical data), illustrating a constant historical appreciation of the franc.

- Recent Stability: For nearly 15 years, the USD/CHF rate has moved within a relatively stable range, mainly between 0.80 and 1.02 USD. This stability contrasts with the movements against the euro.

The evolution of CHF parity shows that it has not only remained strong against historical partner currencies (such as the former Italian lira or the French franc), whose relative value has fallen, but that it continues to appreciate strongly against the dollar and shows great responsiveness to European shocks.

Summary of reasons why the Swiss franc is a strong currency

| Solidity Factor of the Swiss Franc (CHF) | Practical Arguments |

| Safe Haven and Geopolitical Stability | Switzerland has historically preserved remarkable political and social stability. This factor, reinforced by neutrality and an absence of major conflicts, creates a unique capital of trust. In times of uncertainty or global crisis, investors seek to protect their capital, thereby increasing demand for the CHF. |

| Fiscal Discipline and Low Debt | The country maintains rigorous fiscal discipline and a strong will for independence. Switzerland’s low debt ratio (significantly lower than that of its European neighbours) is a major reliability indicator that reassures the markets. |

| Robust Economic Growth and Low Inflation | The Swiss economy demonstrates generally robust growth and has weathered crises without excessive damage. Persistently low inflation and a dynamic economy attract capital, as they preserve the franc’s purchasing power. |

| Role and Independence of the SNB | The Swiss National Bank (SNB) enjoys crucial independence from fiscal policy. Its rigorous, proactive monetary policy aims for price stability. By adjusting the policy rate and actively intervening in the markets (sometimes even acting as an investment fund), it controls and stabilises the value of the CHF. |

| Strategic Reserves (Gold and Currencies) | Switzerland is a major gold holder, maintaining substantial gold reserves. These reserves, combined with foreign currency and securities reserves, reinforce the franc’s credibility. The historical link with gold has helped forge its enduring reputation for stability. |

Swiss franc and foreign capital: a pillar of its stability

Strong currencies attract foreign capital, further reinforcing their value.

The history of the Swiss franc (CHF) is marked by this constant attraction, which is essential to its stability.

Let’s talk about the direct effect of capital flows.

The role of the franc is confirmed in investment movements:

- Massive international flows: Switzerland is a major global financial player. In 2020, it hosted more than CHF 1,216 billion in foreign investment while itself placing more than CHF 1,460 billion abroad.

- Role as a safety valve: In times of crisis, Swiss investors repatriate their funds seeking the safety of the franc.

For example, during 2019 and 2020, more than CHF 88 billion was repatriated. This sudden movement increases demand for the CHF on the foreign exchange markets, acting as an active and immediate support for its value.

The inflow and repatriation of foreign capital are not just an indicator of the CHF’s health; they are an active pillar of its stability. They continually validate the confidence the world places in Switzerland’s political, economic and institutional foundations.

Key takeaways :

The history of the Swiss franc reveals an essential truth: the strength of a currency is always the result of rigorous political choices and constant economic discipline.

The CHF did not become a safe-haven currency by chance.

It was built through unification, the maintenance of the gold standard, the independence of the SNB and proactive crisis management. You now understand the foundations on which this unique solidity rests.

To secure your capital or optimise your exchange transactions with b-sharpe, now use the proven strength of the Swiss franc to your advantage.

Apply this historical knowledge to anticipate movements in the currency market.

On the same topic