Buying a home in Switzerland: what you really need to know before you buy

- Financing your purchase: mortgage, equity and Swiss rules

- Taxation for homeowners: what you gain and what you pay

- Cross-border commuters: buying on the French side or the Swiss side ?

- The exchange rate: the surprise guest in your property project

- Points to watch before signing

- Where to buy and how to go about it?

- Frequently asked questions about buying property in Switzerland

Only 36% of Swiss people own their own homes. The problem? It’s not just the cost of property, but a system with rules that are unique in the world and can quickly become a financial headache. Between the mandatory 20% deposit, the complex tax rules on imputed rental value and the exchange rate trap for cross-border workers, every decision has a significant impact on your budget.

• Want to become a homeowner in Switzerland? Here's what the banks don't explain to you upfront.

• 20% down payment, rental value, interest rate risk: three realities to master before you sign.

• Whether cross-border worker or resident, a few poorly made decisions at the outset can cost you tens of thousands of francs over 20 years.

• The exchange rate is the blind spot of any cross-border real estate project. And that's often where the real savings are made.

- Financing your purchase: mortgage, equity and Swiss rules

- Taxation for homeowners: what you gain and what you pay

- Cross-border commuters: buying on the French side or the Swiss side ?

- The exchange rate: the surprise guest in your property project

- Points to watch before signing

- Where to buy and how to go about it?

- Frequently asked questions about buying property in Switzerland

The good news: with the right strategy, buying a home remains one of the best ways to secure your wealth.

Discover our practical solutions for financing your project, optimising your tax position and avoiding hidden costs.

Let’s take stock.

Buying or renting in Switzerland: the calculation nobody gets right

In Switzerland, the question isn’t simply a matter of comparing rent with a monthly mortgage payment.

The Swiss market has unique rules that radically change the financial side of home ownership.

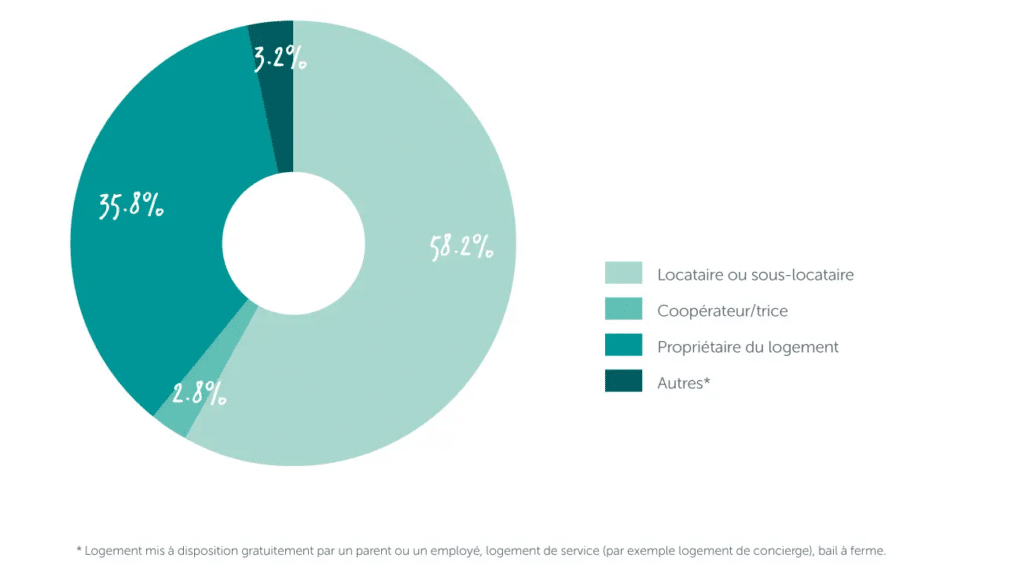

Why only 36% of Swiss people own their own homes

Switzerland remains a country of tenants: nearly 2 homes out of 3 are occupied by tenants.

Source: Federal Housing Office (FHO), Home Ownership, published 26 July 2024

Source: Crédit Agricole – NextBank

This figure is due to the conditions for accessing home ownership being particularly strict compared with other countries.

The main obstacle isn’t just property prices, but the deposit requirement.

To buy your main residence, you must provide at least 20% of the purchase price.

A major additional constraint applies: at least 10% of this deposit must come from your own liquid assets (savings, 3rd pillar, life insurance). The remaining 10% may come from your 2nd pillar (LPP).

Without this starting capital, the project is stuck, whatever your income.

Rent vs monthly repayments: the misleading comparison

Comparing your current rent with your future mortgage repayment is a classic mistake.

While the mortgage repayment often looks lower than the rent, it’s only part of the equation.

Becoming a homeowner brings new costs:

- Maintenance costs: Budget around 1% of the property’s value per year for renovations and everyday wear.

- The imputed rental value: This is a specific tax feature. The tax authorities add a notional income (what you’d save by not paying rent) to your taxable income, which increases your tax bill.

- Purchase costs: Notary fees and land registry fees (around 5% of the price in some cantons such as Geneva) must be paid in cash and aren’t financed by the bank.

The real benefits of home ownership (wealth, security, tax deductions)

Despite the constraints, becoming a homeowner is a powerful lever for securing your future:

- Freedom and security: You’re no longer exposed to the risk of your lease being terminated. You can renovate your home as you please (knock down a wall, repaint) and enjoy complete stability.

- Tax optimisation: In Switzerland, debt is deductible. Your loan interest and maintenance costs reduce your taxable income. If you opt for indirect amortisation (via a 3rd pillar), you can deduct even more tax while paying down your debt.

- Building wealth: Instead of paying rent that’s money down the drain, you invest in bricks and mortar. Historically, Swiss property gains in value, providing security for your old age or a capital gain if you resell.

- Lower costs in retirement: Paying off all or part of your loan before the end of your working life allows you to drastically cut your housing costs just when your income falls.

Financing your purchase: mortgage, equity and Swiss rules

In Switzerland, getting a mortgage doesn’t depend solely on your salary.

The system relies on a strict split between your savings and the bank loan, with calculation rules that can surprise non-residents.

The 20% deposit: where can it come from?

This is the unavoidable entry ticket.

To buy a main residence, you must provide at least 20% of the purchase price as a deposit.

Where this money comes from is strictly regulated:

- The mandatory “cash” portion (10% minimum): Half of your deposit must come from “genuine” liquid assets: bank savings, sale of securities, inheritance, gift, or even your 3rd pillar assets.

- The 2nd pillar (LPP): You can use your LPP, also known as occupational pension assets, to make up the remaining 10%.

- Additional costs: Watch out, the 20% doesn’t cover everything.

You must pay notary fees, transfer duty and land registry fees out of your own liquid assets.

These costs (approx. 5% in Geneva) can’t be financed by the mortgage or by the LPP.

First and second-rank mortgages: how does it work?

Unlike other countries where the whole loan is repaid, Switzerland splits the mortgage into two parts known as “ranks”:

- The first rank (up to 67% of the price): This is the “perpetual” portion.

The bank doesn’t require you to repay it. You only pay the interest. This keeps a debt that’s deductible against your income. - The second rank (the balance, approx. 13%): This is the amortisable portion. It must be repaid within 15 years or, at the latest, when you retire.

💡 Good to know for foreign nationals:

If you hold a B permit, you can acquire your main residence without prior authorisation. For cross-border commuters (G permit), buying a second home is possible without authorisation within the area of your workplace, but it can’t be let out.

Source: FOJ: Acquisition of real estate by persons abroad, factsheet

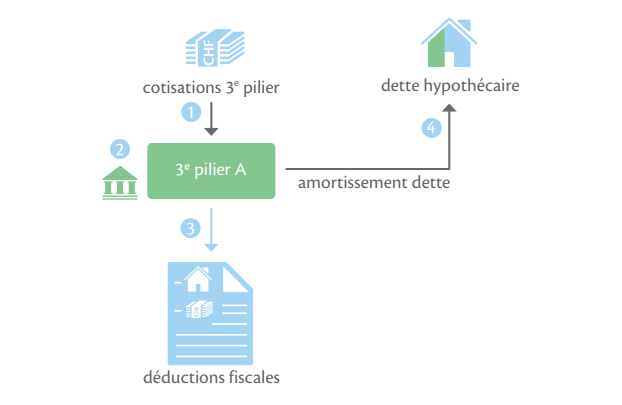

Using your LPP or 3rd pillar to buy: is it a good idea?

Source: BCV brochure – Online Mortgage

Using your pension assets to finance your home is a strategic calculation with two options:

- Early withdrawal: You put the money straight into the purchase. This reduces your debt and your monthly interest, but lowers your future pension benefits and triggers immediate tax on the withdrawal.

- Pledging: Instead of withdrawing the money, you leave it in your pension account. It serves as security for the bank.

The advantage? Your pension capital keeps growing and you retain a higher debt, which maximises your tax deductions.

The Geneva move: if you’re buying in the canton of Geneva, check whether you’re eligible for CASATAX.

If the sale price doesn’t exceed a certain ceiling (CHF 1,394,928 in 2026), you may benefit from a significant reduction on registration duty (up to CHF 20,924) and 50% off the fees for setting up the mortgage. Depending on the amount financed, the total saving can reach up to CHF 27,000. Source: the press release from the Geneva Council of State dated 4 February 2026

💡 The b-sharpe tip :

If your deposit is currently held in euros, the exchange rate can affect your purchasing power at the last minute.

By using a competitive exchange solution to convert your deposit into Swiss francs, you avoid high bank margins and get the most out of every euro invested in your future home.

Taxation for homeowners: what you gain and what you pay

In Switzerland, becoming a homeowner radically changes your tax return.

The system rests on a balance between notional taxable income and deductions that can seriously lighten your tax bill.

The imputed rental value: the tax tenants don’t pay

This is the Swiss quirk that often comes as a surprise: the imputed rental value.

The tax authorities consider that living in your own home gives you an economic benefit equivalent to income.

- How does it work? An amount equal to what you’d earn if you rented out your property is added to your taxable income (generally 60 to 70% of the market rent).

- Reform on the way: A historic decision has been taken to abolish this tax from 1 January 2029 (source: FTA/FDF factsheet on debt interest). It will apply to both main residences and second homes occupied by their owner. In return, most current deductions will be abolished or capped, and cantons will be able to introduce a special property tax on second homes.

💡 Good to know :

An exception is planned for first-time buyers. People buying their main residence in Switzerland for the first time will still be able to deduct part of their mortgage interest for 10 years. The initial cap will be CHF 10,000 for a married couple and CHF 5,000 for a single person, then it will fall by 10% each year.

Source: FDF.

The deductions that offset it (mortgage interest, maintenance, renovation)

To balance out the imputed rental value, the tax authorities let you deduct significant amounts.

This is where you take back control of your budget:

- Mortgage interest: You can deduct almost all the interest paid on your mortgage debt. With the 2029 reform, these deductions will be capped, but today they remain a major tax-saving lever.

- Maintenance and renovations: Work aimed at maintaining the value of your property (painting, replacing a boiler, roof repair) is 100% deductible.

💡 Practical tip :

For small jobs, you can choose the flat-rate deduction (often 10 to 20% of the imputed rental value) without supporting documents. For big projects, opt for actual costs

- Energy efficiency: Investments in installing solar panels or improving thermal insulation are particularly encouraged. They remain deductible and often let you spread the expense over two consecutive tax periods to maximise the impact.

If you’re planning major “upkeep” renovation work, try to schedule it before 2029.

⚠️ Please note : After that date, the abolition of the imputed rental value will come with the disappearance of most deductions for routine maintenance costs.

Cross-border commuters: buying on the French side or the Swiss side ?

When you become a cross-border commuter into Switzerland, where you choose to live is a strategic decision: it affects your quality of life just as much as your long-term financial health.

Between the convenience of being close to Switzerland and the property purchasing power on the French side, here are the key points to help you decide.

The advantages of buying in France on a salary paid in CHF

Buying in France while earning a salary in Swiss francs (CHF) offers an immediate mechanical advantage: much greater purchasing power.

- Price per m²: For the same budget, you get a significantly larger area (often a house with a garden where you’d only have a flat in Switzerland).

- Financing assistance: By buying in France, you may be eligible for schemes such as the Zero-Rate Loan (PTZ), which is unavailable for a purchase on Swiss soil.

- Cost of living: Beyond the credit itself, ancillary costs (insurance, services, upkeep) generally remain lower on the French side, which protects your disposable income.

A loan in euros vs a loan in Swiss francs: the exchange risk over 20 years

This is the crux of the matter for every cross-border commuter. The currency you choose for your mortgage determines your exposure to exchange rate risk for two decades.

- A euro (EUR) loan: This is a bet on the future. If the CHF strengthens against the euro, your monthly repayment costs you “less” in Swiss francs over time.

Conversely, if the euro rises again, your burden increases. - A foreign-currency (CHF) loan: This option removes the exchange risk on your monthly repayments. Since you earn CHF and repay CHF, your burden stays fixed relative to your salary. The catch: the risk shifts to when you resell.

If you sell your property in euros to repay an outstanding balance in Swiss francs, a sharp appreciation of the CHF could force you to inject personal money to clear your debt.

The border areas where you can buy (Haute-Savoie, Ain, Pays de Gex)

The cross-border property market remains very dynamic in 2026, with marked differences by area:

- The Pays de Gex (Ain): Boosted by its proximity to CERN and international organisations, this is a safe-haven area. Towns such as Gex or Divonne-les-Bains remain highly sought after despite prices that have stabilised but stayed high (around €350,000 for a quality two-bedroom flat).

- Haute-Savoie (Annemasse, Saint-Julien): Ideal for those who favour the transport network (Léman Express). It’s the efficient choice for minimising journey times.

- Emerging areas: Looking for more peace and space, cross-border commuters are now moving further out towards the Vallée Verte or towns such as Boëge, where you get better value for money than right on the border.

💡 The right move to save thousands of francs

Whichever loan you choose (EUR or CHF), you’ll need to convert funds.

By using b-sharpe for your monthly transfers or to transfer your deposit, you avoid the inflated exchange rates charged by traditional banks.

Over a 20-year property project, this saving adds up to thousands of francs.

The exchange rate: the surprise guest in your property project

If you earn your living in Swiss francs (CHF) but are buying in euros (EUR), or vice versa, the exchange rate becomes a major player in your transaction.

Ignoring its impact means accepting a loss of several thousand euros without even realising it.

Deposit, monthly repayments, notary fees: 3 moments when currency exchange gets expensive

Buying a property breaks down into stages where the need for currency is critical:

- The deposit transfer: This is the largest amount sent in a single go. On a deposit of €100,000, a rate difference of just 1% between two providers means a €1,000 gap. That’s an amount that could cover part of your moving costs or your new appliances.

- Purchase costs (notary): Often wrongly called “notary fees”, these mainly include transfer duty and taxes paid to the State. These costs must be settled by transfer before the deed is signed. An unfavourable exchange rate when converting these tens of thousands of euros needlessly inflates the final bill.

- Loan repayments: This is the “drop by drop” impact. Over a 20-year loan, saving just €15 a month thanks to a fairer exchange rate means a total gain of €3,600. It’s the easiest saving to make in the long run.

On amounts like these, it’s worth comparing margins before choosing your currency exchange provider.

What b-sharpe actually changes in a property transaction

Using b-sharpe rather than a traditional bank transforms the financial management of your purchase:

- Complete transparency: Unlike banks, which often apply a “daily” rate that’s unknown when you start the transfer, b-sharpe lets you see the exact rate before confirming your transaction.

- Zero hidden fees: For large property-related transfers, bank commissions can quickly add up. b-sharpe cuts out these middlemen to offer an extremely competitive exchange rate, very close to the market rate.

- Speed and security: Notaries require funds to be available in their client account before they can sign the deed. b-sharpe guarantees fast, secure transfers, essential for meeting legal deadlines and not delaying your move.

We’re not a bank, we’re your currency exchange partner.

Our aim is to give you back control over your multi-currency money by sparing you excessive margins.

For your property project, every penny saved on exchange is one more investment in your future home.

Points to watch before signing

Buying property in Switzerland is a marathon, not a sprint.

Between market pressure and long-term financial commitments, several points deserve particular attention so that your dream doesn’t turn into a burden.

Scarce supply and pressure on prices

The Swiss market is characterised by supply that is structurally lower than demand, especially in urban centres (Geneva, Lausanne, Zurich).

A tight market

The scarcity of building land and population growth are keeping prices at record levels. In 2026, finding that “rare gem” requires quick reactions and a financing application already pre-approved by your bank.

The competition

You’re not alone. There are many buyers with substantial personal funds (inheritances, LPP capital withdrawals). To stand out, the strength of your personal deposit (often above the 20% minimum) is your best argument.

The hidden costs of home ownership (charges, renovations, insurance)

The sale price is only the tip of the iceberg.

Being a homeowner brings recurring costs that tenants never see:

- The renovation fund: If you buy under condominium ownership (PPE), you must contribute monthly to a fund set aside for future work on the building (roof, lift, façade).

- Routine maintenance: The golden rule is to set aside 1% of the property’s value every year to cover repairs and natural wear. For a property worth CHF 1,000,000, that’s CHF 10,000 a year.

- Insurance: Buildings insurance (compulsory in most cantons) and life/disability insurance (often required by the bank to cover the debt) add to your monthly outgoings.

Interest rate risk: what happens if mortgage rates rise again?

Most Swiss buyers opt for long-term fixed rates (10 or 15 years) to protect themselves.

Source: BCV brochure – Online Mortgage

But interest rate risk remains a reality when your loan comes up for renewal:

The financial shock

If your rate goes from 1.5% to 3.5% at the end of your fixed-rate term, your monthly repayment can double.

It’s crucial to calculate your borrowing capacity using a theoretical rate of 5% (used by banks) to make sure you can always pay, even in a crisis.

The SARON strategy

Some people choose variable rates based on SARON.

This is often more cost-effective, but it requires financial resilience capable of absorbing sudden rises in the cost of borrowing.

💡 Advice from our experts :

Don’t let unexpected costs eat into your budget.

By optimising your currency exchange when paying your bills (if you live between two countries) or when building up your renovation savings, you free up financial room to cope with any rate increases.

Where to buy and how to go about it?

Successfully carrying out a property project in Switzerland calls for method and good local knowledge.

Here are the resources and key steps for turning your dream into reality.

The best cities to invest in for 2026

The Swiss market isn’t limited to Geneva.

In 2026, several hubs stand out for their dynamism and yield potential:

- Zurich: The economic capital remains the most dynamic and international market, ideal for the security of the investment.

- Lausanne: A safe bet, driven by its university hub (EPFL, UNIL) which guarantees steady rental demand.

- Neuchâtel & Fribourg: These cantons are gaining visibility thanks to entry prices that are more affordable than on Lake Geneva’s shores, offering attractive gross yields (around 4.2%).

- Valais (Sion, Martigny): An area in full economic development, boosted by improved rail links. Read our detailed analysis: Property: where to invest in Switzerland?

The complete purchasing process in 3 steps

In Switzerland, the journey is marked out by strict steps designed to protect both parties:

- Preparation (financing): Confirm your budget by calculating the 20% deposit and applying the 33% rule (your housing costs must not exceed a third of your gross income).

- The offer and the contract: Once you’ve found the property, you sign a notarised sales contract and usually pay a 10% deposit (held in escrow).

- The deed of sale: This is the final moment when the notary formalises the transfer of ownership and registers it in the land registry. See our step-by-step guide: How to buy a property in Switzerland?

Surrounding yourself with the right experts

Buying a property is a complex operation that needs trusted partners:

Estate agencies

Whether you’re looking for the transparency of a digital agency like Neho or the local roots of networks such as Naef or Barnes, choosing the right middleman is decisive. See our selection: The best Swiss estate agents

The notary

Essential, they’re the legal guarantor of the transaction. Their presence is required to draft the deed and register it in the land registry. See our directory: The best Swiss notaries

At every stage that involves moving funds (deposit, balance of the price, notary fees), remember to plan ahead for your currency exchange needs.

Our solutions let you settle these amounts in the currency of your choice, without incurring bank margins.

Key takeaways :

Becoming a homeowner in Switzerland is a demanding life project that leaves no room for improvisation.

To succeed, you need to master your deposit, plan ahead for the 2029 tax changes and, above all, protect your purchasing power. Don’t let banks eat into your property budget.

Whether for your initial deposit or your monthly repayments, every currency exchange matters.

Ready to take the leap? Simulate your savings with b-sharpe and make the most of every franc invested in your future home.

Frequently asked questions about buying property in Switzerland

In Switzerland, banks’ golden rule is the affordability ratio.

Your theoretical housing costs (interest calculated at a prudent rate of 5%, amortisation and 1% maintenance costs) must not exceed 33% of your gross annual income.

Practical example: For a property worth CHF 1,000,000 with a deposit of CHF 200,000, a household income of around CHF 180,000 is generally required to secure financing.

Yes, but under certain conditions.

If you hold a G permit and have worked in Switzerland for more than six months, you can acquire a second home in the region of your workplace without prior authorisation.

For your main residence, however, you must physically live there, which often means changing your status to a residence permit (B permit).

Yes, this is a widely used lever.

You can withdraw or pledge your LPP assets to build up your deposit.

Note, however, that the law requires at least 10% of the purchase price to come from “genuine” own funds (savings, 3rd pillar, cash) not sourced from the 2nd pillar.

What’s more, any withdrawal will reduce your benefits at retirement.

Beyond the monthly repayment, budget for:

• The imputed rental value: A notional income added to your taxes (being phased out from 2029).

• Condominium charges (PPE): Including the mandatory renovation fund.

• Maintenance: Around 1% of the property’s value to set aside every year.

• Taxes: Property tax (depending on the canton) and compulsory insurance.

There’s no single answer, it all depends on your priority:

• Buying in France: You get greater purchasing power and larger spaces, but you’re exposed to exchange rate risk over 20 years and longer commutes.

• Buying in Switzerland: You gain stability (salary and loan in the same currency), proximity, and you build wealth in a strong currency, but the initial deposit is much harder to raise.

When transferring your deposit or repaying your monthly instalments, avoid standard bank transfers, which apply inflated exchange rates (often 1.5 to 2.5% margin).

By going through a currency exchange specialist such as b-sharpe, you benefit from transparent rates close to the market rate.

On a property transaction, this simple decision can save you several thousand francs, immediately usable for your works or your furnishings.

On the same topic

The best estate agents in Switzerland