Bring your savings home: exchange your CHF at the best rate

Are you leaving Switzerland and want to repatriate your 3rd pillar pension or your personal savings? With b-sharpe, you can transfer your funds securely from Geneva at market rates.

Secure transfer

Competitive rates

Swiss customer service

Bring your savings home without cutting into your savings

A 3rd pillar pension or Swiss savings account usually amounts to tens of thousands of francs. When transferring funds abroad, a bank margin of 1–2% on the exchange rate can cost you hundreds, or even thousands, of francs.

With b-sharpe, your savings are converted at the market rate, with a commission known in advance and dedicated support from Geneva.

Your savings are for your future. Not bank margins.

How do you transfer

your Swiss savings?

Receipt and conversion of your funds

When your insurer or provider releases your funds (3rd pillar or personal savings), your assets are paid into a personalised IBAN in your name, generated by b-sharpe.

With b-sharpe, you can:

• receive your funds securely in Geneva,

• convert them into the currency of your choice at market rates,

• track every step from your personal account.

Every transaction is monitored in accordance with Swiss security and compliance standards.

Secure transfer to your overseas account

Once your assets have been converted, they can be transferred to the account of your choice (bank account, solicitor, insurance company, etc.).

With b-sharpe, you can:

• send your funds without opening a local account,

• benefit from a fast transfer, with fees known in advance,

• receive support from a team of Swiss experts every step of the way.

Our aim: to ensure every franc of your savings goes towards your plans.

When and how

should you withdraw your savings?

You are retiring outside Switzerland

- Pillar 3a savings can be withdrawn up to five years before reaching retirement age.

- A departure certificate is required, and the credit is subject to withholding tax.

You are moving to live outside the EU/EFTA

- It is possible to withdraw all your savings (Pillar 3 and Pillar 2).

- A certificate of departure is required, subject to specific tax rules.

You are leaving Switzerland before retirement (EU or EFTA)

- Pillar 3a savings (or voluntary savings) can be withdrawn by providing a certificate of departure.

- Part of the 2nd pillar remains frozen in a vested benefits account.

You consolidate your assets before departure

- Your 2nd pillar can finance the purchase under the EPL scheme, subject to your pension fund’s rules.

- Centralising them simplifies administrative management and reduces the costs associated with international transfers.

Swiss security. The speed of a fintech company.

Your conversions and transfers go through a secure Swiss system with no hidden surprises. You remain in control at every stage, from the first click to the receipt of funds.

A Swiss IBAN in your name

No more copying payment references. Transfer your funds just as easily as you would with a traditional bank account.

A 100% Swiss service

A secure solution and a Geneva-based team, serving you since 2013.

Save money on every transaction

Our rates are among the most competitive on the market. Everything is disclosed in advance, so you know exactly how much you will receive.

Over 40,000 satisfied clients

With an average rating of 4.8/5 on Trustpilot

They have tried b-sharpe

and recommend it

“Quick, good exchange rates and no fees. I hadn’t yet found a way to transfer my Swiss francs back to my euro account in France, but now I have.”

18 February 2025

Like thousands of individuals and businesses, exchange your currency at the best rate with b-sharpe.

✓ Verified review

Excellent

Top-notch service! Money transfers are incredibly efficient, fast and, above all, the cheapest on the market. The customer service is second to none: responsive, professional and really friendly. The customer experience manager even called me to explain how to set up a personalised IBAN: a real bonus! I’d recommend them in a heartbeat.

3 June 2025

4.8/5 on Trustpilot

Over 3,000 verified reviews, not just empty promises

Bringing your Swiss

savings home has never been easier.

- Create an account

- Sending funds

- Delivery within 24

hours, excluding weekends and public holidays

- NO account opening fees

- NO account management fees

- NO account closure fees

Everything you need to know about repatriating

Swiss savings

Find out how to manage your currency conversions and international transfers with ease. Clear and concise articles to help you streamline your international transactions.

Pillar 3: should you withdraw or continue contributing to it after leaving Switzerland?

How do I make an international money transfer?

A closer look at the Swiss LPP for cross-border workers

Frequently asked questions about

repatriating savings

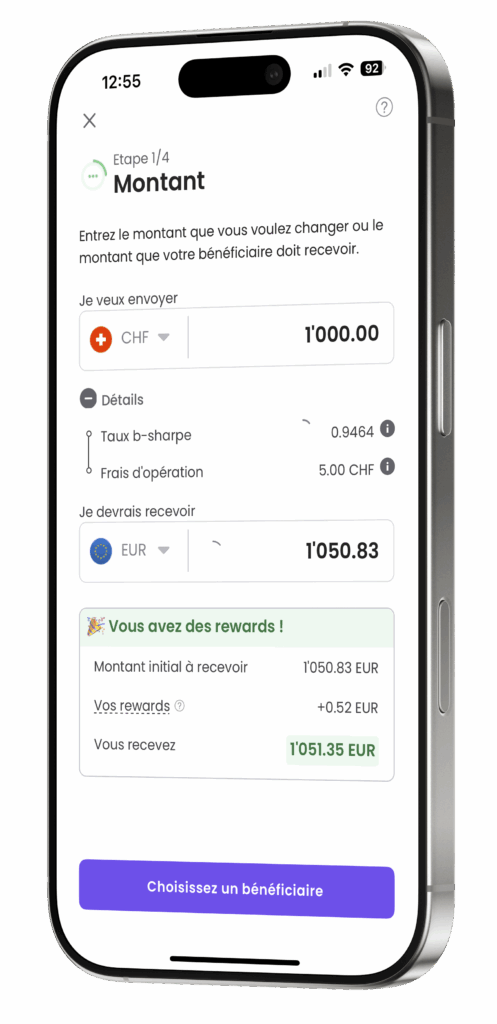

The fees depend mainly on the cost of converting the currencies involved. At b-sharpe, the market rate and transaction fees are displayed before confirmation, allowing you to know the exact cost of the transaction, with no hidden fees included in the rate.

Once your funds have been received in your b-sharpe IBAN, the conversion and transfer to your destination account are completed within 24 to 48 working hours, depending on the currencies involved. The entire process, from registration to receipt of funds, can be completed in one to two working days.

With b-sharpe, you can create a free online account, transfer your savings in CHF to your Swiss b-sharpe IBAN from your bank, and specify your foreign bank account as the destination. Your funds are converted at the market rate and transferred to your foreign currency account within 24 to 48 working hours, from Geneva, with no intermediaries.

Yes, withdrawal of your 3a pension is permitted if you leave Switzerland permanently. To do so, you must provide a certificate of departure issued by the cantonal authorities.

Withdrawing after departure can sometimes offer more favourable tax treatment. However, depending on your host country, it may be better to withdraw the funds beforehand. Find out more to optimise your situation.

Withholding tax is deducted by the pension fund at the time of payment. Depending on tax treaties, a tax credit may apply in your country of residence to avoid double taxation.

Yes. You can keep your 3a pillar contract even after leaving Switzerland. The funds remain locked in until an event occurs that allows for withdrawal (retirement, property purchase, etc.).