2024 Financial Review: Is the battle against inflation over? Have central banks finally achieved their targets?

The year 2024 was marked by a number of events that had a direct impact on the global economy and the financial markets.

• In 2024, the SNB surprised markets with bigger-than-expected rate cuts (-0.25% three times), backed by successful control of inflation.

• The ECB also cut rates three times (from 4.5% to 3.15%), while the dissolution of France's National Assembly weighed on financial markets (CAC down 11.5%).

• A tense geopolitical backdrop (Middle East, Russia-Ukraine war) continued to weigh on markets throughout the year.

The SNB: spot-on or indecisive?

The first event worth mentioning took place here in Switzerland. Throughout the year,

we saw a series of surprise rate cuts announced by SNB President Jordan.

The Swiss National Bank has on three occasions announced interest rates that were lower than investors had expected, specifically in March, June and December, when rates were set 0.25% lower than forecast.

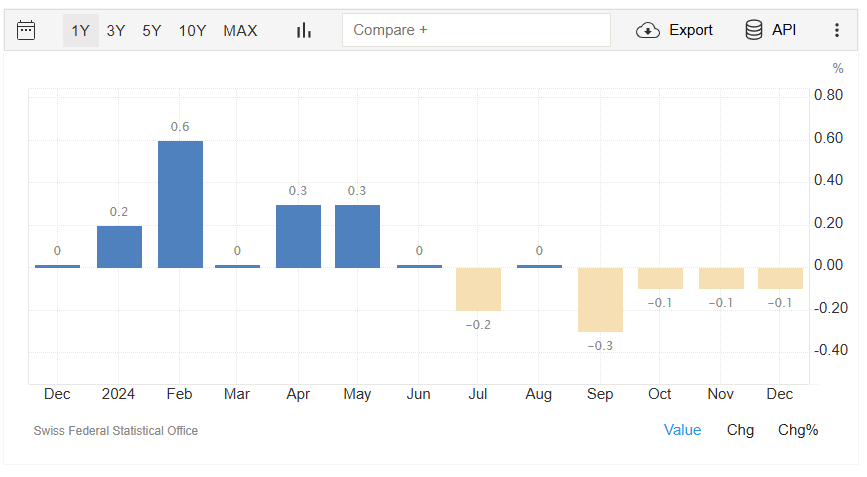

This willingness to take risks in order to surprise the markets with unexpected rate cuts can be explained by the SNB’s complete control over inflation. We can see that, despite these unexpected rate cuts, Swiss monthly inflation has been falling steadily over three of the four quarters.

Europe is doing well, but France isn’t

Like her American and Swiss counterparts, the President of the European Central Bank, Ms Lagarde, began to ease monetary policy by cutting interest rates from June onwards.

Although less confident than Mr Jordan about bringing inflation under control, the ECB has nevertheless cut interest rates three times this year, from 4.5% to 3.15%, whilst keeping monthly inflation between 2.9% (January 2024) and 2.2% (December 2024).

Another key issue in 2024, which has had a greater impact on Europe, and particularly on France, is the dissolution of the National Assembly announced on 9 June 2024 by French President Emmanuel Macron

The President has decided to dissolve the National Assembly, partly in response to the presidential party’s poor showing in the European elections and the rise of the National Rally.

The main consequences of this event in France are as follows: the suspension of pending bills, the calling of new general elections and, above all, the appointment of a new Prime Minister. Following Gabriel Attal’s resignation in September, François Bayrou was appointed to the post on 13 December.

Another consequence of the announcement of the dissolution of the National Assembly is the poor state of the French financial markets.

The CAC, which has struggled to perform since March 2024, saw its index fall by nearly 11.5% at its lowest point following the announcement, dropping from 7,903 to 7,030.

Geopolitical conflicts remain as intense as ever

The year 2024 was also marked by various geopolitical conflicts, including those in the Middle East and the Russia-Ukraine war, which had a significant impact on the health of the global economy.

An unexpected return?

To round off these various points, we must mention one of the most significant events of 2024: the election of Donald Trump on 5 November 2024 as President of the United States for the second time in three terms.

Even though the future US president will not take office until January 2025, no market has been left unscathed.

One of the future president’s key pledges is fiscal stimulus, in the form of tax cuts and tariff reductions, designed to support the health of local businesses, which should, in theory, lead to favourable growth for the stock market

The US S&P 500 index rose by nearly 5.3% in the week following the announcement and has continued to climb throughout the year, eventually breaking through the $6,000 mark.

Although he has not yet taken office, Donald Trump has wasted no time in appointing his loyal supporter, Elon Musk, to head the “new US Department of Government Efficiency”.

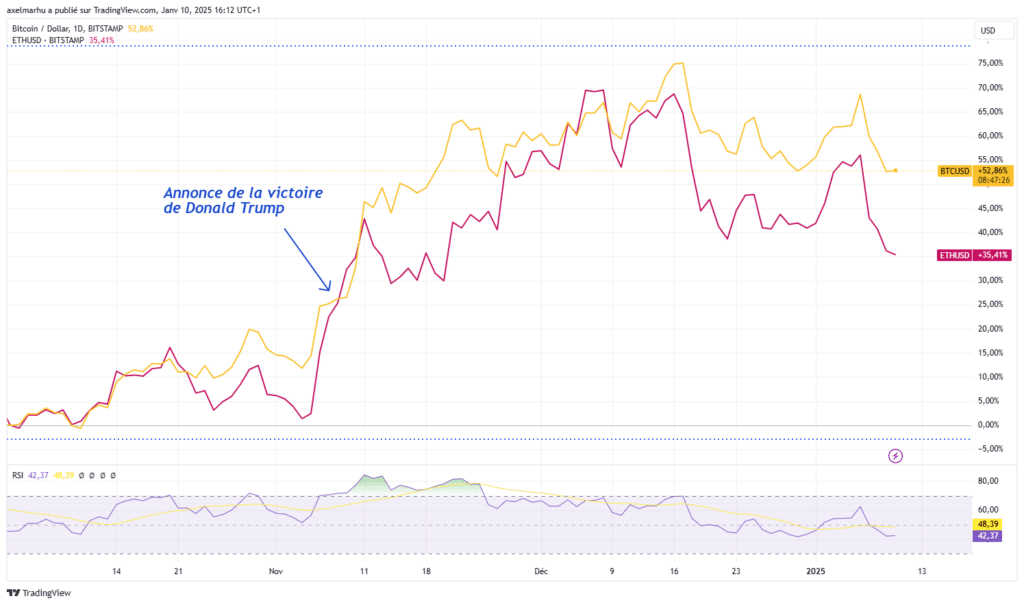

One market in particular has capitalised on this announcement to outperform the rest, and that is the cryptocurrency market.

Given billionaire Elon Musk’s interest in this asset, Trump’s announcement that he intends to appoint Musk to a government post will almost certainly lead to better legislation and a policy more conducive to the development of cryptocurrencies.

The most famous cryptocurrency, Bitcoin, has risen by more than 60% at its peak, even reaching the long-awaited $100,000 mark, since Trump’s election, and other cryptocurrencies have taken the opportunity to skyrocket. (+70% for Ethereum, +200% for Dogecoin – I can’t list them all, as that would take me several hundred hours).

What about currencies in all this?

Since 1 January 2024, the EUR/CHF currency pair has had some (pleasant?) surprises in store for us. It has been almost two years since the exchange rate reached parity, which is a historic milestone.

Whilst most forecasts pointed to a return to parity, the EUR/CHF has been unpredictable and has failed to meet these expectations. At best, we have seen a rise of +6.92% since 1 January, reaching a high of 0.9930 in 2024. The currency pair did not fall completely either, depreciating by a maximum of -0.81% to reach an all-time low of 0.9201.

From a technical perspective, one area in particular has caught my attention. This is the zone between 0.9480 and 0.9580. Throughout 2024, this zone has acted as both support and resistance, having been tested and rejected a total of five times.

In 2024, the first significant event occurred on Monday 5 August, a day on which global financial markets suffered a sharp fall (down 3% on the S&P 500 and down 12.65% on the Nikkei), and which subsequently became known as ‘Black Monday’.

Secondly, a few months later, on Friday 22 November, we hit the current all-time low of 0.9201.

Since the beginning of October, the EUR/CHF market has been trading within a range between 0.9440 and 0.9270 and has not yet decided whether to continue its downward trend or stage an upward retracement.

What does the future hold for 2025?

The year 2025 is fast approaching, and here are just a few of the many issues that could have a significant impact on the financial sector, and the Forex market in particular.

Trump

Trump’s return to the limelight on 20 January signals yet another year that is likely to be full of twists and turns. Between the introduction of tariffs, his desire to put the United States back on the ‘right track’ and his outlandish remarks (such as when he suggested that Canada should become the 51st US state), the financial markets as a whole (stock indices, foreign exchange, equities, bonds, commodities, cryptocurrencies) are set to be shaken up. We anticipate high volatility.

And in Europe?

In Switzerland

Swiss inflation is rapidly approaching 0.5%, whilst the SNB continues to try to surprise the market by cutting key interest rates by slightly more than expected. The question on everyone’s lips is: will we see negative interest rates again by 2025 to counter the strong Swiss franc and low inflation? One thing is certain: the new SNB President (Martin Schlegel) has not ruled out a return to negative rates. Watch this space…

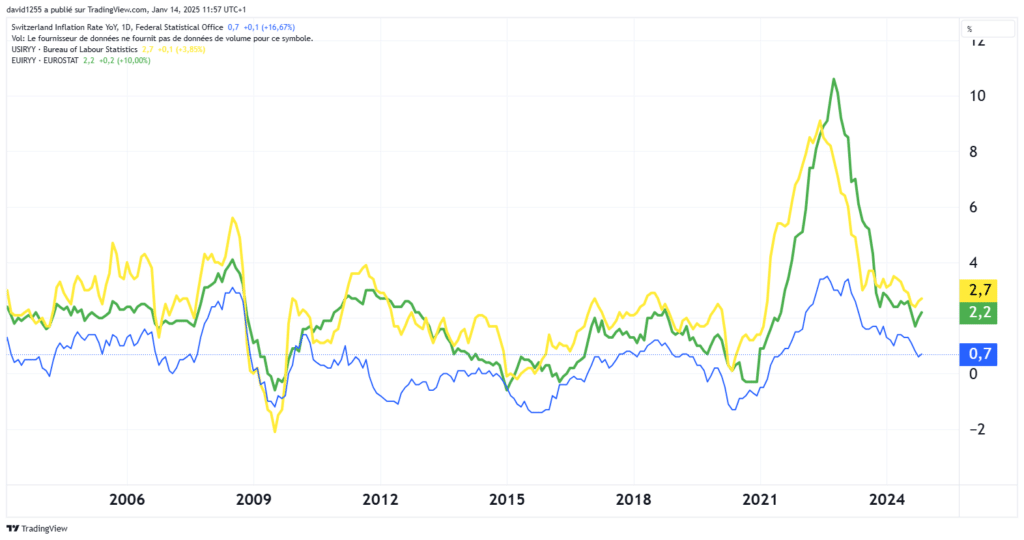

Here is the annual inflation rate for the eurozone (green), the United States (yellow) and Switzerland (blue). As you can see, Switzerland has never been particularly affected by this figure, thanks to the Swiss franc, which has helped to curb the import of inflation into our country.

In Germany

Europe is at a major turning point, with political tensions in France and in Europe’s leading power. Indeed, Germany has endured two years of recession, with the car industry struggling. Volkswagen plans to close factories in Germany. This highlights just how badly one of the key sectors of the German economy is suffering. Added to this are the snap elections due to take place in February. German Chancellor Olaf Scholz lost a confidence vote in the Bundestag in December 2024. The centre-right opposition leader stands a chance of being elected during what he describes as one of the greatest economic crises in post-war history…

On the same topic