The Swiss franc: the history of a strong currency turned safe haven

A strong currency and a safe haven investment, the Swiss franc (CHF) is key to the exchange market. Find out more about its history and main advantages.

With a strong economy, low debt, and sizable foreign investment, today all the ingredients are there to make the Swiss franc a strong currency and a safe haven investment.

The strength of the Swiss franc isn’t new. Today’s Swiss franc draws as much strength from Switzerland’s economic relations with its main partners as from its history.

As a currency exchange business, b-sharpe considers the origins of the Swiss franc’s strength so you can better understand how the currency market works.

Exchange your money quickly and securely

What are the differences between a strong currency and a weak currency?

The notion of a currency’s strength is entirely relative. A currency can be strong in relation to one currency, and weak in relation to another.

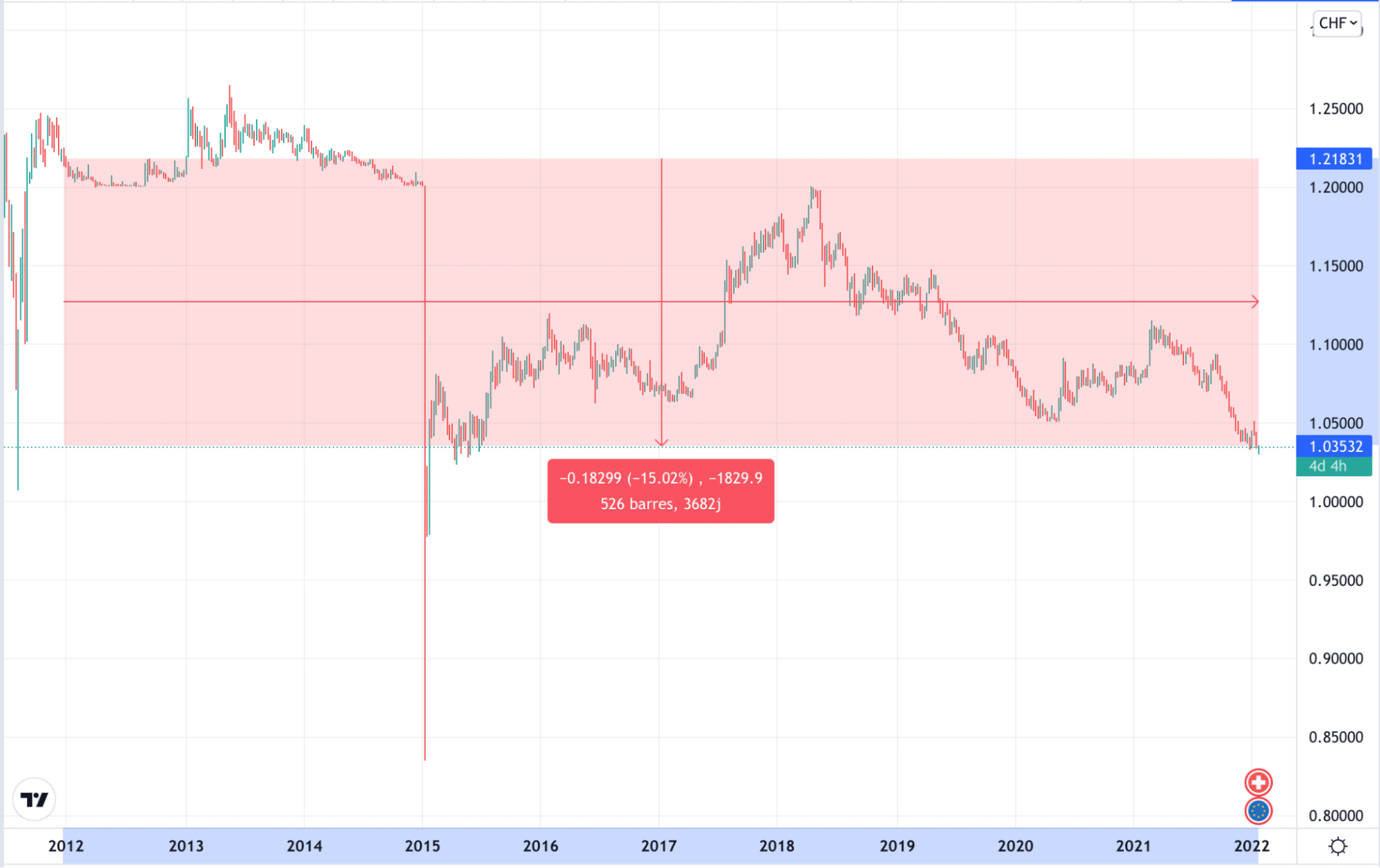

Let’s take the EUR/CHF pair as an example (i.e. what one euro is worth after being exchanged into Swiss francs). At the start of 2012 you would have to spend around 820 Swiss francs to buy 1000 euros – but today you would have to spend 966 Swiss francs to obtain the same amount.

If we take it as read that we are dealing with two strong currencies here, the Swiss franc has won over the euro in the last decade with a positive exchange rate development compared to the single currency.

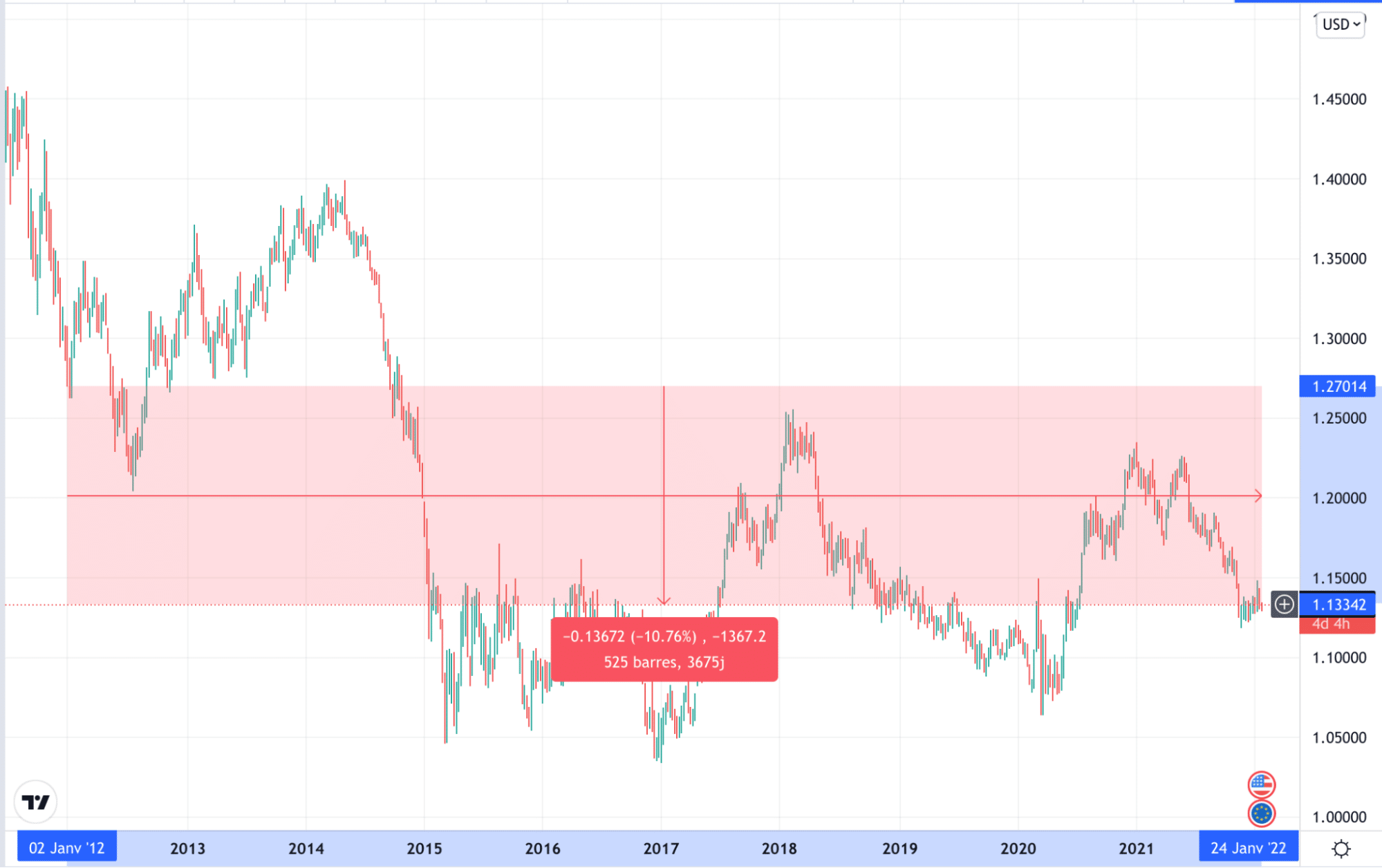

Let’s take another example over the same period. You had to spend about $1270 to get €1000 in 2012, but today you can spend a little less, $1134 to obtain the same sum.

The Swiss franc in the 20th century

From the 1920s to the Second World War

During the 1920s, European currencies collapsed one after another climaxing with the German mark. The victim of a period of hyperinflation in the Weimar Republic where retail prices increased from a factor of one to 750 million in the matter of a decade. In real terms, a loaf of bread that sold for 1 mark would cost 750 million marks ten years later – illustrating the currency’s loss of value!

On the contrary, Swiss currency kept its safe-haven value because it maintained its gold standard, attracting increasing amounts of foreign investment.

At the end of the 1920s, the high price of the Swiss franc didn’t bode well: the Swiss exporter economy felt the full force of the costly Swiss franc. Unemployment affected over 20% of the active population in the middle of the 1930s.

During the Second World War, Switzerland amassed gold stocks by selling raw materials to Germany in exchange for the precious yellow metal.

The Swiss franc built its solid foundations over these 25 years.

Switzerland and the Bretton Woods agreement

At the end of the war, Switzerland refused to adhere to the Bretton Woods agreement (which set currencies in relation to the dollar fixed to gold), but the Swiss franc remained one of the strongest currencies.

The Bretton Woods system ended in 1971. Currencies became free-floating (i.e. currency rates were driven by supply and demand) and the Swiss economy was in good health. Foreign capital flowed into Swiss banks, although Swiss businesses, particularly the industrial sector, experienced more difficult times and unemployment increased in Switzerland.

The 1970s petrol crisis and the financial crisis of the 1990s

The petrol crisis of the 1970s put an end to the Swiss National Bank’s plans to suppress the growth of the Swiss franc. The difficult economic situation in Switzerland continued with poorly executed liquidity injections into the economy aimed at reducing the effects of the 1987 crash.

This resulted in the construction and property sectors beginning to overheat. To counter this, the SNB increased interest rates, plunging the country’s economy into a deep recession. The 1990s would end up being very difficult economically because of a delayed drop in interest rates. However, the Swiss franc remained steady against almost all other currencies.

The floor rate as a response to the 2008 crash

To deal with the fallout from the 2008 crash, in 2010 the SNB decided to lower interest rates to zero to protect the Swiss banking system and flood the market with liquidity.

Despite this, the Swiss franc retained its role as a safe haven investment and its rate grew significantly against the euro and the dollar. This led the SNB to implement a floor rate against the euro (to protect Swiss exports). This continued until the EUR/CHF floor rate came to an end suddenly in 2015.

Why the Swiss franc is a strong currency

In Switzerland’s case, two key factors explain the robustness of the Swiss franc compared to other currencies:

- economic growth; when considered in an international context, also it has emerged from the most recent crises without suffering too much damage.

- low levels of debt; despite the crisis, Switzerland’s indebtedness is a lot lower than its European counterparts. Swiss debt levels are under 30% of GDP, while those of its neighbours have soared to 116.3% in France and 153.5% in Italy.

- Geopolitical stability. Unlike some currency areas that are relatively unstable because of geopolitical factors and/or galloping inflation, Switzerland remains reassuringly stable from an economic and political point of view.

Switzerland, the Swiss franc, and foreign capital

Countries with a so-called strong currency always possess the same characteristic: they attract foreign investment capital. The more foreign capital flows in, the stronger a currency becomes.

In 2020, there were more than 1,216 billion Swiss francs of foreign investment in Switzerland. In light of this, Switzerland invested over 1460 billion Swiss francs worldwide.

Switzerland is a country that invests most abroad. But in 2019 and 2020, in the context of the pandemic, its businesses repatriated respectively 54 and 34 billion Swiss francs which supported the Swiss franc on the exchange market.

Is the Swiss franc a safe haven?

According to a study published by the French organization CEPII, the Swiss franc may not be in such a strong position. To back this up, it analyzed the behavior of the principal currencies during crises. Starting with the assumption that a safe haven must bring a positive return during periods of crisis and a negative risk premium in the long term.

On this basis, analysts examined the behaviour of 26 currencies over the15 years 1999–2013. To their surprise, according to the terms of the analysis only two currencies behaved like a safe haven.

On the contrary, the Swiss franc, which tends to follow the movement of the euro, did not demonstrate the characteristics of a safe haven. However, the analysts did say that the analysis was before the end of the EUR/CHF floor rate. It is possible that free from being indexed to the euro, the Swiss franc will progress more favorably during a period of crisis.