Everything you need to know about exchange rates

3 points to help you understand how exchange rates work.

• The interbank rate is the reference rate at which banks exchange currency with each other; it is never directly accessible to individuals or businesses.

• Each intermediary (bank, bureau de change, online service) applies its own margin to this reference rate, which explains the gap of several percent seen between providers.

• On the same amount exchanged, a lower margin translates directly into more money received — comparing providers before converting remains the best reflex.

1 – What is the interbank exchange rate?

The interbank rate essentially reflects the value of one currency against another when two banks exchange them. This rate fluctuates constantly in line with the law of supply and demand.

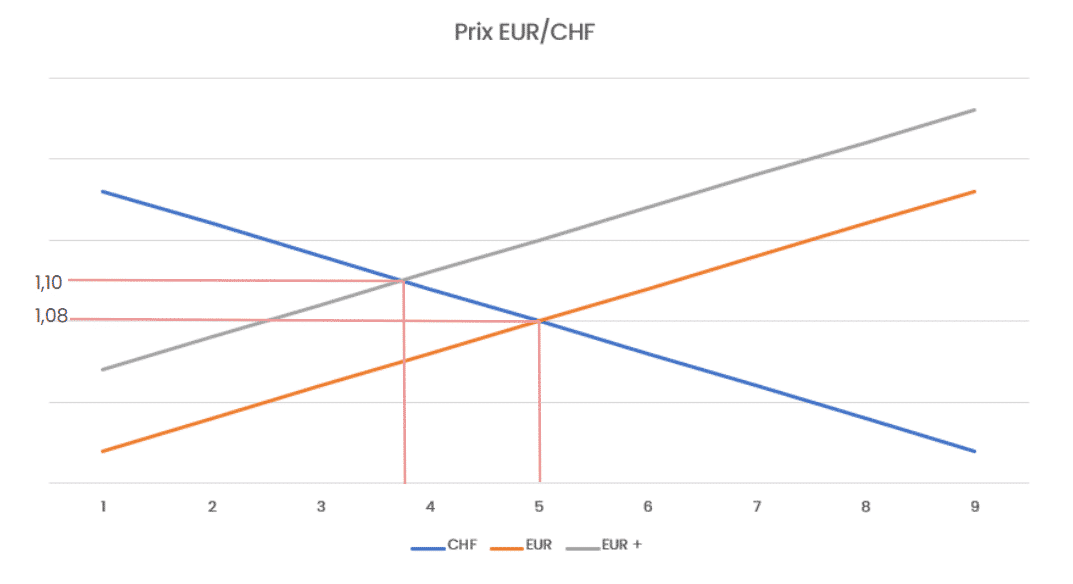

For example, when we talk about EUR/CHF, we are referring to the exchange rate or interbank rate between the euro and the Swiss franc. In this case, if the interbank rate is 1.10, this means that for one euro, the market will pay you 1.10 francs.

As this market is based on supply and demand, this means that it will fluctuate depending on the number of buyers and sellers.

For example, if the banks (and market participants through them) decide to buy large amounts of euros in exchange for francs, the exchange rate will rise. In other words, for one euro, you will no longer get 1.08 CHF but 1.10 CHF.

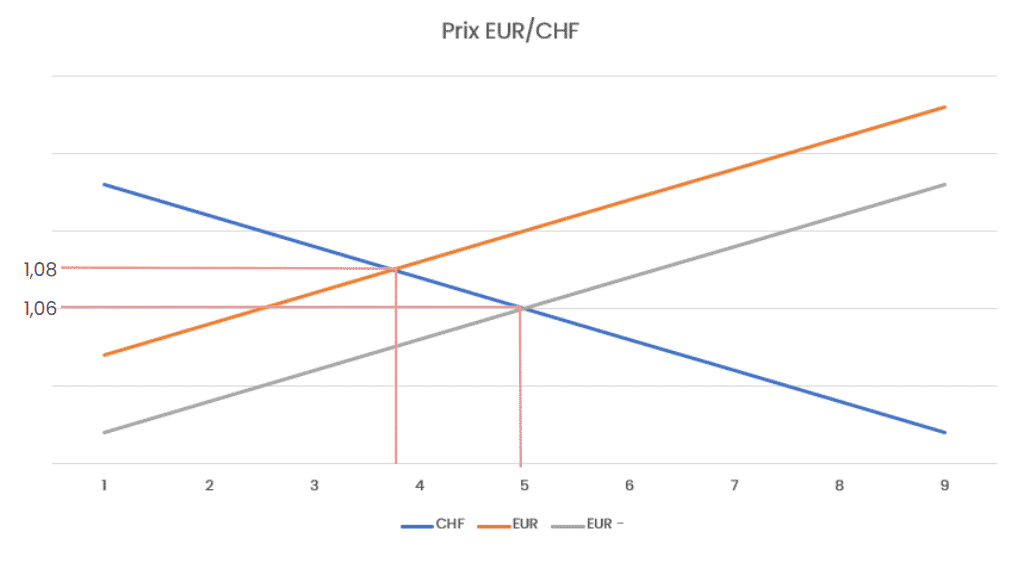

Conversely, if there are many sellers of the euro, the EUR/CHF exchange rate will fall; in other words, for one euro you will no longer get 1.08 CHF but 1.06 CHF. The price is therefore a compromise between the sellers and buyers of a currency and is governed by the laws of supply and demand.

The number of buyers or sellers fluctuates constantly. This can be influenced by a range of external factors, such as a trade agreement, a war, a peace treaty, a general election, a health crisis or any other news that might affect investors’ decisions.

However, the interbank exchange rate is merely a reference figure rather than a rate at which you can actually carry out a transaction. No one, whether an individual or a company, can access this rate outside the banking system. The rate offered to other users is inevitably subject to a mark-up, the size of which depends on the individual financial intermediary.

2 – How does the margin on my trade work?

Whenever you carry out a foreign exchange transaction – whether it’s a credit card payment in a different currency, a foreign exchange transaction through your bank, or via an intermediary such as b-sharpe – a margin is applied to the exchange rate.

This refers to the fee paid to the intermediary carrying out the transaction. This margin can range from a few basis points to several per cent, depending on the amounts involved and the intermediaries involved in the transaction. It is often very difficult to obtain information about the margin applied prior to a transaction.

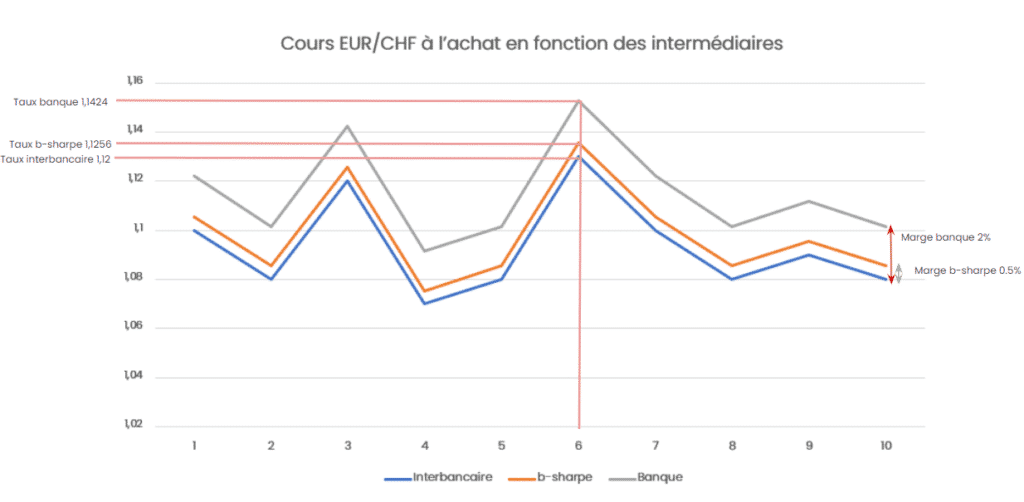

We can, however, estimate the margin applied in general terms. For a transaction of CHF 10,000 into euros: local banks apply a margin ranging from 1.5% to 2%, physical bureaux de change apply a margin ranging from 0.75% to 0.9%, and online intermediaries such as b-sharpe apply a margin of 0.5%.

Based on these factors, the rate applied to your transaction can be calculated as follows: Intermediate rate = Interbank rate × (1 + intermediate margin), as follows:

If the interbank rate = 1.12

Bank rate = 1.12 × (1 + 0.02) = 1.12 × 1.02 = 1.1424

Spot exchange rate = 1.12 × (1 + 0.009) = 1.12 × 1.009 = 1.1301

b-sharpe rate = 1.12 × (1 + 0.005) = 1.12 × 1.005 = 1.1256

As the rate changes constantly, this can be illustrated by the graph below:

3 – How much money will I receive?

To know at any given time how many euros you will receive from a Swiss franc to euro conversion, you simply need to understand the mechanism explained above. The EUR/CHF exchange rate, which is calculated by your broker and fluctuates constantly, essentially means: ‘I will have to pay XX.XX CHF to get 1 euro.’

If we take the previous example again, with an interbank rate of 1.12 and 10,000 CHF, here is the calculation to use to work out how many euros you will receive, depending on the intermediary used:

With your bank:

- Bank rate = 1.12 × (1 + 0.02) = 1.12 × 1.02 = 1.1424

- Amount: CHF 10,000

- Amount received = 10,000 / 1.1424 = €8,753.50

Through a physical currency exchange broker:

- Spot exchange rate = 1.12 × (1 + 0.009) = 1.12 × 1.009 = 1.1301

- Amount: CHF 10,000

- Amount received = 10,000 / 1.1301 = €8,848.77

With b-sharpe:

- b-sharpe rate = 1.12 × (1 + 0.005) = 1.12 × 1.005 = 1.1256

- Amount: CHF 10,000

- Amount received = 10,000 / 1.1256 = €8,884.15

The difference in the amount received is solely due to the margin applied to the transaction. Please note, however, that as the interbank rate fluctuates constantly, this calculation is based on a rate at a given point in time (T) that is the same for all intermediaries.

Furthermore, if the transaction is to be carried out not from CHF to € but from € to CHF, the principle remains the same; however, the interbank rate must no longer be multiplied but divided, and the amount sent must be multiplied by this rate as follows:

If the interbank rate = 1.12

b-sharpe rate = 1.12 / 1.005 = 1.1144

This means that for every €1 sent, you will receive 1.1144 CHF; so for €10,000, you will receive 10,000 × 1.1144 = 11,144 CHF.

You can find all our margins at: https://www.b-sharpe.com/en/how-it-works/

On the same topic