Online

currency exchange Favourable rates, no hidden fees

Exchange your currency online with the rate displayed before each conversion. It’s quick, requires no bank visits and is cheaper than your bank.

Account-holder’s IBAN

Customer service in Geneva

No hidden fees

Download the app directly onto your smartphone

5 ★ out of 28 reviews

4.4 ★ out of 156 reviews

A fair rate for every conversion

Between hidden fees and mark-ups on exchange rates, the currency exchange services offered by banks often lack transparency. As a result, you end up paying far more than expected to convert your funds.

b-sharpe applies the actual interbank rate and a reduced commission, which is always disclosed in advance. You have full control over your conversion costs and benefit from a secure service based in Switzerland.

Exchange your currency

with b-sharpe in 4 steps

Create your b-sharpe account

You can sign up online in just a few minutes. Your account will be activated within 24 working hours, with no sign-up fees or commitment required.

Please specify the destination account

Please provide the account details for the account that will receive the converted funds: this can be one of your own accounts or that of a relative (parent, child, spouse, brother or sister).

Fix the exchange rate

Lock in the b-sharpe rate directly via the platform or with one of our advisers. The rate is guaranteed for 48 hours.

Send the funds

Make a bank transfer from your bank to your Swiss b-sharpe IBAN. Once we receive the funds, we will convert them and transfer them to the destination account within 24 working hours.

Create your b-sharpe account

You can sign up online in just a few minutes. Your account will be activated within 24 working hours, with no sign-up fees or commitment required.

Please specify the destination account

Please provide the account details for the account that will receive the converted funds: this can be one of your own accounts or that of a relative (parent, child, spouse, brother or sister).

Fix the exchange rate

Lock in the b-sharpe rate directly via the platform or with one of our advisers. The rate is guaranteed for 48 hours.

Send the funds

Make a bank transfer from your bank to your Swiss b-sharpe IBAN. Once we receive the funds, we will convert them and transfer them to the destination account within 24 working hours.

How does online currency

exchange work?

Currency conversion

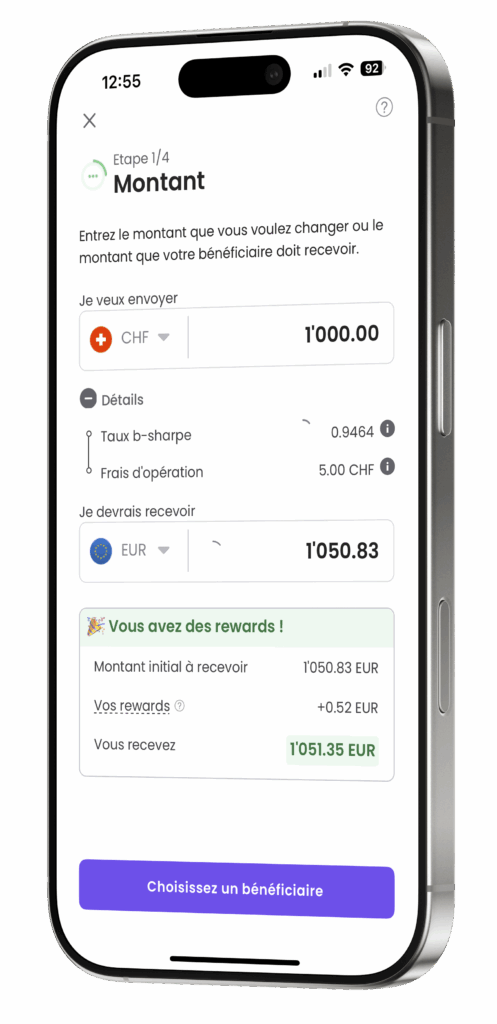

When you send your funds, we apply the market rate, which is displayed before you confirm the transaction. Fees are clearly stated, with no hidden mark-ups.

You know exactly how much you will receive in your chosen currency.

This process ensures there are no nasty surprises:

• the market rate is displayed before the conversion,

• fees are shown in advance,

• the final amount is visible before confirmation.

The transfer of your converted funds

Once the conversion is complete, the funds are transferred to your bank account in the currency of your choice.

The process is quick and complies with Swiss security standards.

No local account is required: you simply receive the money wherever you wish.

Our aim is to make your currency exchange clear, simple and free from unpleasant surprises.

When should you exchange

your currency with b-sharpe?

Would you like to transfer your Swiss salary (CHF to EUR)?

- By no longer paying a bank margin of between 1% and 2%, you can limit the losses on each pay cheque.

- When you convert your funds, the exchange rate used is the market rate, plus b-sharpe’s transaction fees (from 0.12%).

Are you thinking of withdrawing your 2nd pillar pension?

- By transferring your pension savings to the b-sharpe scheme, you can avoid high bank fees.

- Everything is clear and easy to read. This allows you to be sure of the amount you will actually receive.

Are you planning to finance a property purchase?

- Converting a large sum at the reduced B-Sharpe rate reduces the overall cost of the transaction.

- A clear rate allows you to secure the necessary budget for your project.

Whether it’s for a purchase, a project or a specific situation, you can convert the amount you need into the currency of your choice.

Swiss reliability. The speed of a fintech company.

Your conversions and transfers go through a secure Swiss system with no hidden surprises. You remain in control at every stage, from the first click to the receipt of the funds.

A Swiss IBAN in your name

No more copying payment references. Transfer your funds just as easily as you would with a traditional bank account.

A 100% Swiss service

A secure solution and a Geneva-based team, serving you since 2013.

Save money on every transaction

Our rates are among the most competitive on the market. Everything is disclosed in advance, so you know exactly how much you’ll receive.

Over 40,000 satisfied customers

With an average rating of 4.8/5 on Trustpilot

They have tried b-sharpe

and recommend it

“A super-simple and intuitive service for exchanging currencies at the best rates! I save several hundred francs every year.”

12 December 2025

Like thousands of individuals and businesses, exchange your currency at the best rate with b-sharpe.

✓ Verified review

Excellent currency exchange service

Very fast transfers, very fair exchange rates – I’m blown away by this highly efficient service, which makes life so much easier for anyone with multiple currencies and bank accounts. My only regret is not having discovered it sooner!

19 December 2024

4.8/5 on Trustpilot

Over 3,000 verified reviews, not just empty promises

Exchanging currency

has never been easier.

- Create an account

- Sending funds

- Delivery within 24

hours, excluding weekends and public holidays

- NO account opening fees

- NO account management fees

- NO account closure fees

Everything you need to know

about currency exchange

Find out how to convert and transfer your funds abroad with ease. Clear and concise articles to help you optimise your international transactions.

Pillar 3: should you withdraw or continue contributing to it after leaving Switzerland?

How do I make an international money transfer?

A closer look at the Swiss LPP for cross-border workers

Frequently

asked questions about online currency exchange

b-sharpe uses the market rate (interbank rate) at the time of your transaction, plus a commission clearly stated before confirmation. The rate displayed on the interface is the one that will actually be applied to your conversion.

The fees take the form of transaction charges starting at 0.12%; these are applied to the actual interbank rate. The amount you see displayed includes this commission, so you can be sure of the amount you will receive if you decide to lock in the rate.

Once your funds have been received, b-sharpe carries out the conversion and then transfers the funds to your bank account in the chosen currency. In most cases, the conversion and transfer take a few days. The exact time may vary depending on your bank and the destination country. We will keep you informed of the main stages of your transaction.

b-sharpe is a Swiss company subject to local anti-money laundering requirements, affiliated with SO-FIT, a recognised self-regulatory body in Switzerland. Client funds are held in segregated accounts with leading partner institutions. Internal controls and technical security measures are in place to protect your currency exchange transactions.

An online currency exchange service allows you to buy and sell currencies via a digital platform, with the exchange rate displayed before confirmation. At b-sharpe, you send funds to your personal Swiss IBAN, choose the time of conversion, and the amounts are then transferred to your foreign currency accounts. You also have the option of receiving assistance from an expert on our team, who can be reached by phone.

There is no minimum amount required to use b-sharpe. However, as the rates are generally more favourable for larger amounts, it is often better to avoid making too many small transactions in order to optimise the overall cost of the exchange.